Lululemon

Disclaimers

This is not investment advice. Do your own research

I bought 34 shares at a cost basis of $295.65

I don’t care if you buy

I exited this position in the low $300s as I found more obvious opportunities and also changed my mind about how hard retail is.

Retail at a glance

Retail fashion is one of the hardest businesses to analyze. While the basic premise of the business is fairly straightforward (put clothes in a store and sell them) it’s difficult to read into both their current and future success. This is largely to do with the fact that fashion often falls into two categories: Fad or Fashion Brand. I think we can all go back through our memories of the various fads we participated in our youth. Being emo is definitely not a phase Mom (Etnies anyone?). Many of these companies will see massive adoption of their products and as a result strong financial results in their quarterly earnings reports. Everything looks good until that group gets older and grows out of the fashion trend. Suddenly that brand is old and used and the company sees a decline. This is a story as old as time and you can actually read about some of Warren Buffet’s forays into clothing retail from his 1970s shareholder letters (hint: it didn’t go well). So the question is, is Lululemon just a fad or is it a brand?

Why do you buy an iPhone over an Android?

I only use my phone for email, internet browsing, messaging and occasionally music. I’m 100% confident that the various alternatives to the iPhone perform all of these functions just as well at a lower cost but I will still shell out $1,000 for the new iPhone when my current phone inevitably breaks. That’s because I know what the Apple brand represents: innovation, quality, exceptional user experience and a seamless ecosystem. As a user I am willing to pay a premium for that. So why do people pay $100 for a pair of Yoga pants? The same reason people buy an iPhone over an Android, the brand experience. This leads to an interesting caveat in the fashion world: more luxury products are rarely fads and as a result a different business. Premium clothing is more fad-resistant because of its high-quality materials, strong brand heritage, exclusivity and loyal customer base. Lululemon knows this and it’s why they have done quite well.

What is the Lululemon Brand?

Lululemon is 100% vertically integrated which means they are responsible for the entire process of design, production and sales. What's notable is they only sell their products through their store and Amazon. As a result they have complete control over brand presentation. They don’t do any B2B, which means their products don’t end up on the sales floor of Walmart for instance. Their product is known as athleisure and they are one of the pioneers in the field. It’s a great balance between practical workout clothing that is also functional and flattering. This is great for busy folks who need to get s*** done, be comfortable and occasionally get a workout in. Additionally they have brand ambassadors for each store. These are everyday people, often Yoga instructors. These ambassadors are real and attainable, which is a stronger selling point in today’s world of realistic and body positive imaging. It’s a bit different from Nike’s advertising campaign who prefer to use someone like Michael Jordan. Michael Jordan was a world class athlete, but none of us will reach that level of athleticism. Lululemon is also sold at an expensive price point, many of their clothes go for $100+ with great quality. This does give the premium feel to their brand which is important. Everyone wants Lululemon but not everyone can have it.

The Competition and risks

Lululemon has two main competitors: Vuori and Alo Yoga Pants.

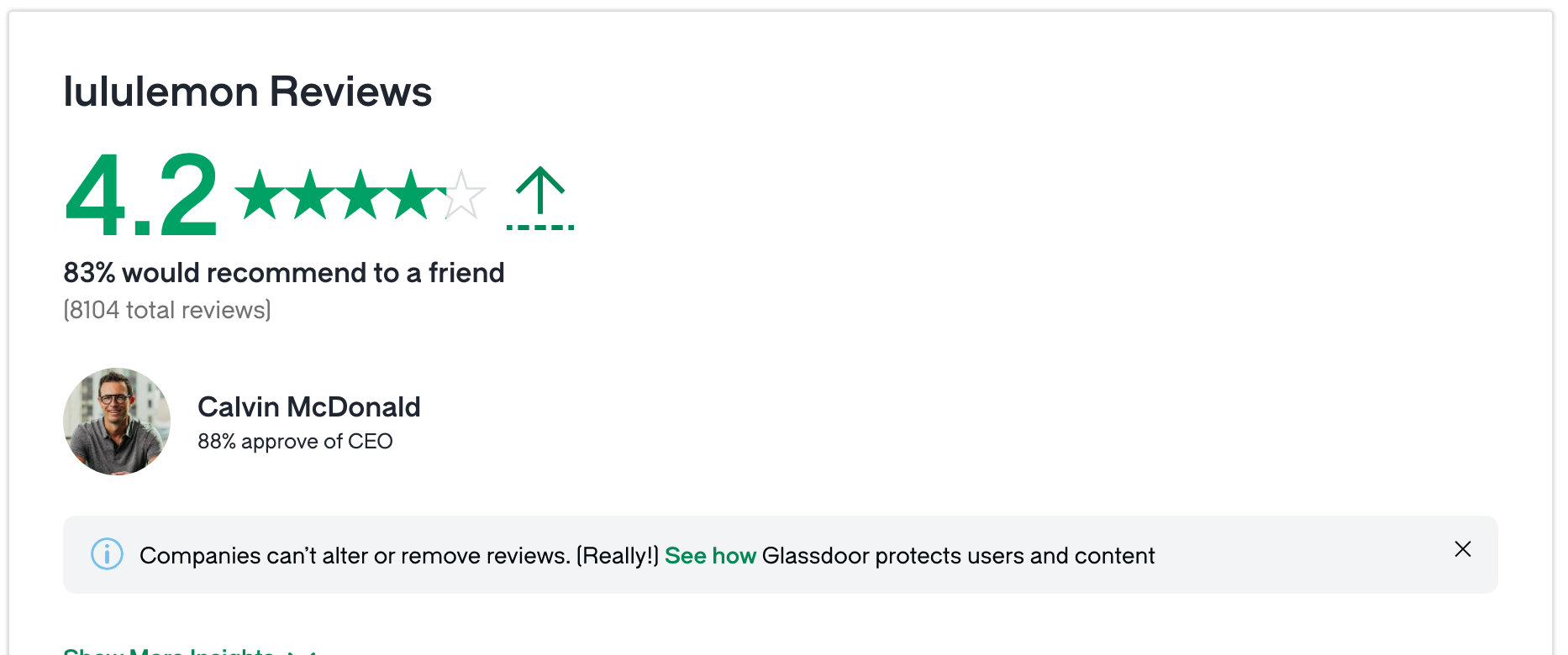

I do not see Alo as much of a threat and it is largely due to their Glassdoor. I don’t use Glassdoor as a hard signal, but reading through it, I can tell the company is not a great place to work. Their CEO has a 48% approval rating, that’s the lowest I have ever seen. Many of the comments are about the toxicity of the workplace. In general, it’s hard for a company to succeed long term under bad leadership and unhappy employees. From what I also can find online a lot of folks feel Alo is the same price point with lower quality. It seems Alo is great for loungewear but not as strong in terms of functionality. Additionally I’ve noticed that while their instagram boasts 3M followers they don’t have much engagement, averaging 1k likes a post. Lululemon’s follower count of 5M tends to average 10k+ pretty consistently. I’ve also noticed their subreddit is also much smaller at 5k users to Lululemon’s 500k. Alo is solid but definitely trailing.

Vuori is of genuine quality and it’s clear to me that people who want more luxury athleisure wear will either shop at Vuori or Lululemon. From what I can find online people often shop at both. It tends to come down to variance in style and occasional difference in quality. One thing I have noticed is their user engagement is significantly less. They have a subreddit of 5k relative to Lululemon’s subreddit of 500k. Their instagram is at 750k relative to Lululemon’s 5m. In general I would coin them as the smaller upstart that is sharing the marketplace with Lululemon. My prediction is they will grow alongside each other and share the space. I think Vuori has to either put out higher quality products for the same price or significantly distinguish their products to take large market share from Lululemon. I don’t see Lululemon losing out to Vuori long term due to the strength of Lululemon’s culture and leadership. Lululemon as it stands is still a much stronger brand than both of their competitors.

Another concern is that a lot of their production and supply is in Asia. In general the typical geographic risk with China exists here. I can’t give you anything helpful to assuage fears on China. I do think instability in China would tank the entire market for what it’s worth.

Finally, the last risk is that Lululemon really is just a fad. When a fad dies it hurts a company immensely and they have to go through the cycle of being out of favor for a while. If I am wrong about the premium brand thesis, we will see a reduction in the business of Lululemon here in the next few years. The real question you should ask yourself before buying this business is the one I posed above: is it a fad or fashion brand?

The Numbers

People really like working at Lululemon and they also really like the CEO. I give Lululemon a solid check for leadership and employee culture.

Net income and their strong margins

Revenue Growth

Historical P/E compared to other publicly traded sports wear companies

Lululemon has never not grown revenue in their 20+ years of being a publicly traded company representing a CAGR of about 28% for revenue

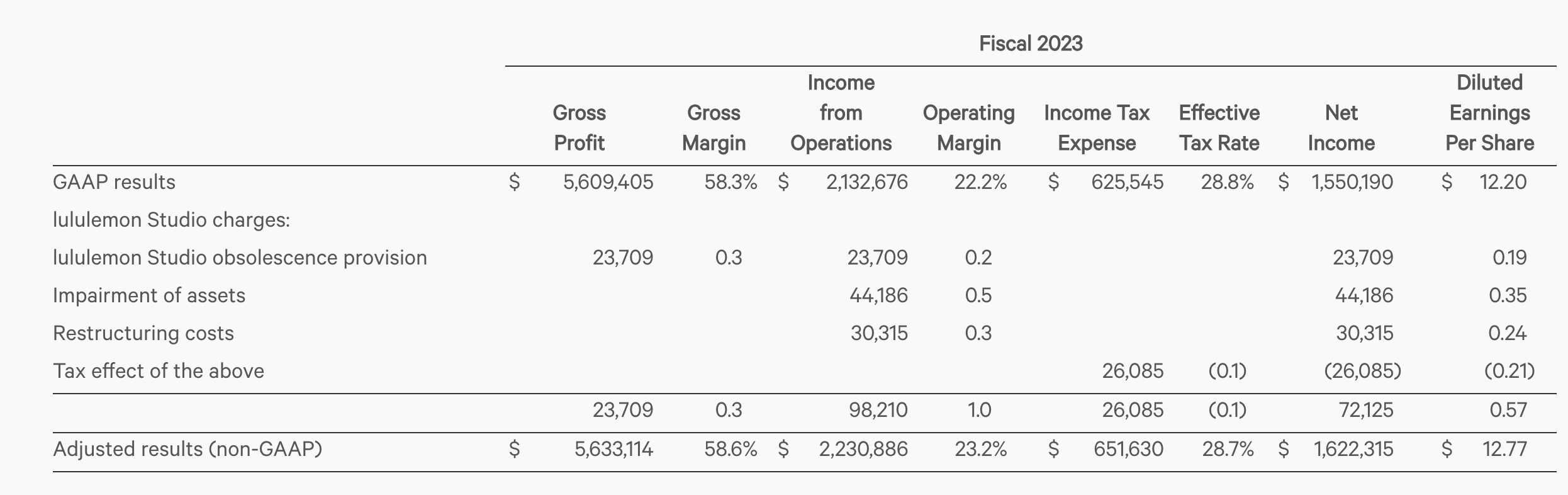

Net income of $1.5B for the 2023 fiscal year. They’ve compounded this at about 47% annually. I don’t expect them to maintain that rate, and think probably 10-20% annually is much more likely.

They have $2.2B in cash with 0 debt. At their current price I hope they are doing significant buybacks.

Since 2015 their diluted shares outstanding has been reduced every single year through share buybacks. A reduction of about 11% in the shares outstanding have driven EPS from $1.66 to $12.22

Their gross margins are insanely good at 58%, on par with Google and well above the industry average of 50% or less. This is because they charge more and spend less on advertising compared to their competitors.

Americas revenue growth from 2021-2022 was 28% and from 2022- 20223 it was 11.9%. China Mainland revenue growth from 2021 - 2022 was 32% and from 2022 - 2023 it was 67%. Rest of the world revenue growth from 2021- 2022 was 29.6% and from 2022 - 2023 it was 42%

Also to note, the executive team only owns .5% of the company. They don’t have major skin in the game like a founder led company would. With that being said, they are all required to have at least 3x of their base salary held as stock while they work there. CEO is at 5X. It’s not as much as I would like, but it does mean they have the properly aligned incentives here.

The reason Lululemon’s price has been beaten up a bit is because their growth in the Americas was 9% YoY in their first quarter of 2024. But their international growth is astounding at 54% YoY. It’s clear to me any decline in the Americas will be offset by their international growth. Going through their numbers they are the best in the business on every metric. Additionally the Chief Product officer Sun Choe announced her departure. She has been there since 2016 and I honestly just see this as a change of pace for her. No company should fail because of the loss of one person. Given their historical excellence, I fully believe they will be fine long term. The only complaint I have was their $500m acquisition of mirror in 2020. To date it has been a complete flop and total write off. Big bets do need to be made, so I hope it was a learning experience for them and we don’t see this bad of an acquisition again. With that being said, the numbers to keep track of going forward is their international growth and domestic growth. I would like to see revenue maintain its pace of 10%+ a year and I want to see international sales continue growing like a weed at 30%+ a year. Then any net cash should be used to do buybacks as long as the share price remains favorable. If they execute this, the reset of the numbers follow.

Conclusion

Mohnish Pabrai often says younger people have a massive advantage in investing because they are more attuned to the new and upcoming companies. As a teenager I loved Chipotle, EA (fifa) and Facebook. All companies that did well. It’s obviously anecdotal but the numbers confirm what JoeMoguss is saying here and who Lululemon appeals to, higher end customers. My general thesis is that Lululemon is a premium athleisure brand with strong customer loyalty. As a result I feel their business will continue to grow in all markets, especially internationally. Their current P/E of about 25 is at a 7 year low, making their price quite attractive. The ONLY reason I can think to not buy this company is because it is retail fashion. I believe this will likely be the first and last retail fashion company I ever buy. It’s quite rare to find a brand this strong, with numbers this strong trading at a price this cheap in the retail fashion world. As for the future price, I don’t have a prediction or a DCF. I know that seems strange but in this instance my investment is based on buying an excellent company at a good price, especially relative to their publicly traded competitors. I believe in the company and in the product, so I will let them do their thing and compound my money for me. I hope to achieve at least 10% CAGR, but as always only time will tell.