SoFi

Disclaimers

This is not investment advice. Do your own research

I don’t own any SoFi stock currently and I don’t care if you buy the stock

This is a beefy article, so buckle up

A necessary disclaimer

To be fully transparent, I have been skeptical about SoFi from the beginning, largely due to their association with Chamath Palihapitiya. I highly encourage all to read this article to learn more about the upstanding character of Chamath. SoFi went public through a SPAC (special purpose acquisition company). If you are not familiar with SPACs I recommend you read this. It’s an alternative form of going public as opposed to the traditional route. SPACs essentially allow companies to bypass the typical due diligence process that is required in a traditional IPO. As a result you and the investor are likely investing in a company with iffy financials. The reason companies might IPO via a SPAC is that they are a better guarantee for cash infusions but also limit the amount the company going public can make. So typically a company with strong financials will not opt to go public through a SPAC. Historically SPACs have underperformed and today I want to take a closer look at SoFi to help investors understand the future potential of this business.

SoFi

SoFi’s primary goal is to help their customers achieve financial independence. This is not the traditional sense of financial independence where you retire early, but instead, they seek to provide each individual with all the financial tools they need to succeed in life. Their core businesses are lending, technology platform, and financial services. Throughout this article, we will dissect each segment, breaking down its contributions in terms of revenue and explaining what each segment does.

Because SoFi trades at a premium, my focus will be on growth specifically in revenue since ultimately that’s the number that counts the most in a growth company. Before we go deep on these key segments we need to discuss two KPI’s that SoFi keeps track of and why we will be ignoring them entirely.

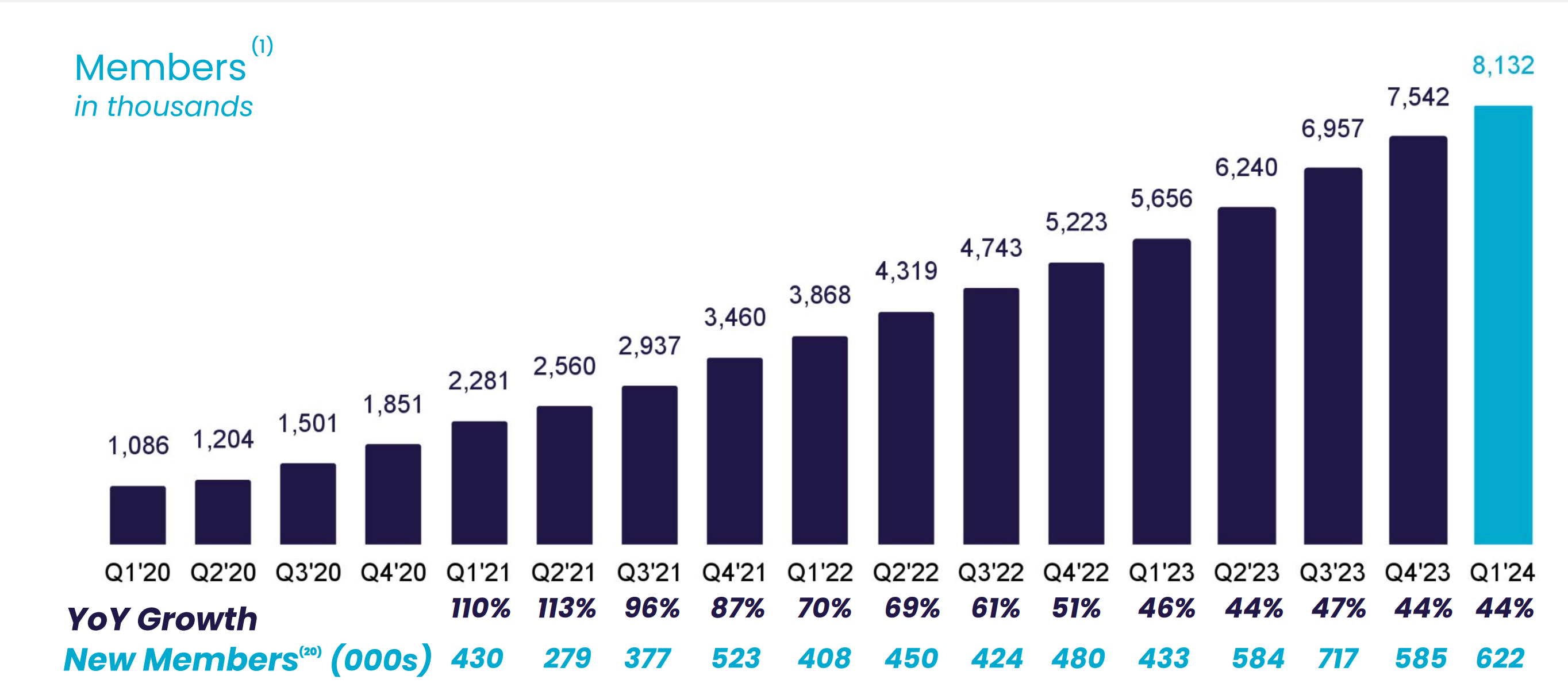

SoFi Members

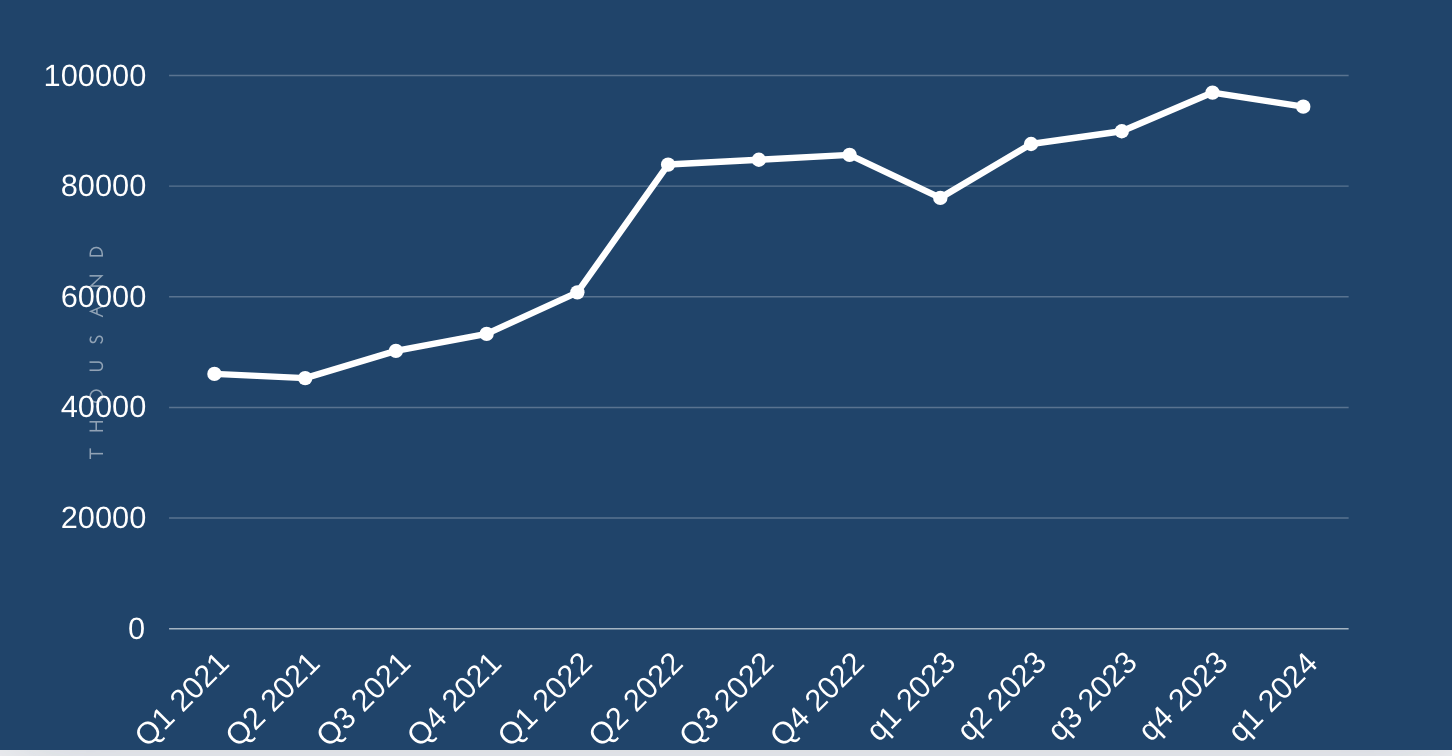

A SoFi member is anyone who has a lending relationship with SoFi through origination and/or ongoing servicing, opened a financial services account, linked an external account to their platform or signed up for their credit score monitoring service. Essentially if you use a SoFi product then you are counted as a member. Once someone becomes a member, they are always considered a member unless they violate SoFi’s terms of service. Essentially if you sign up for a product but are no longer active you are still counted as a member. This is important to understand as it means their numbers should be taken with a grain of salt. This metric would be a lot more meaningful if it was the number of active members. There’s really no point in tracking members if they aren’t active unless you want to pump your numbers. Because this metric is obscured, we will be ignoring it since it requires too much guess work. Below you can see their member growth. If all these members are active it’s impressive, if not, then it’s significantly less impressive.

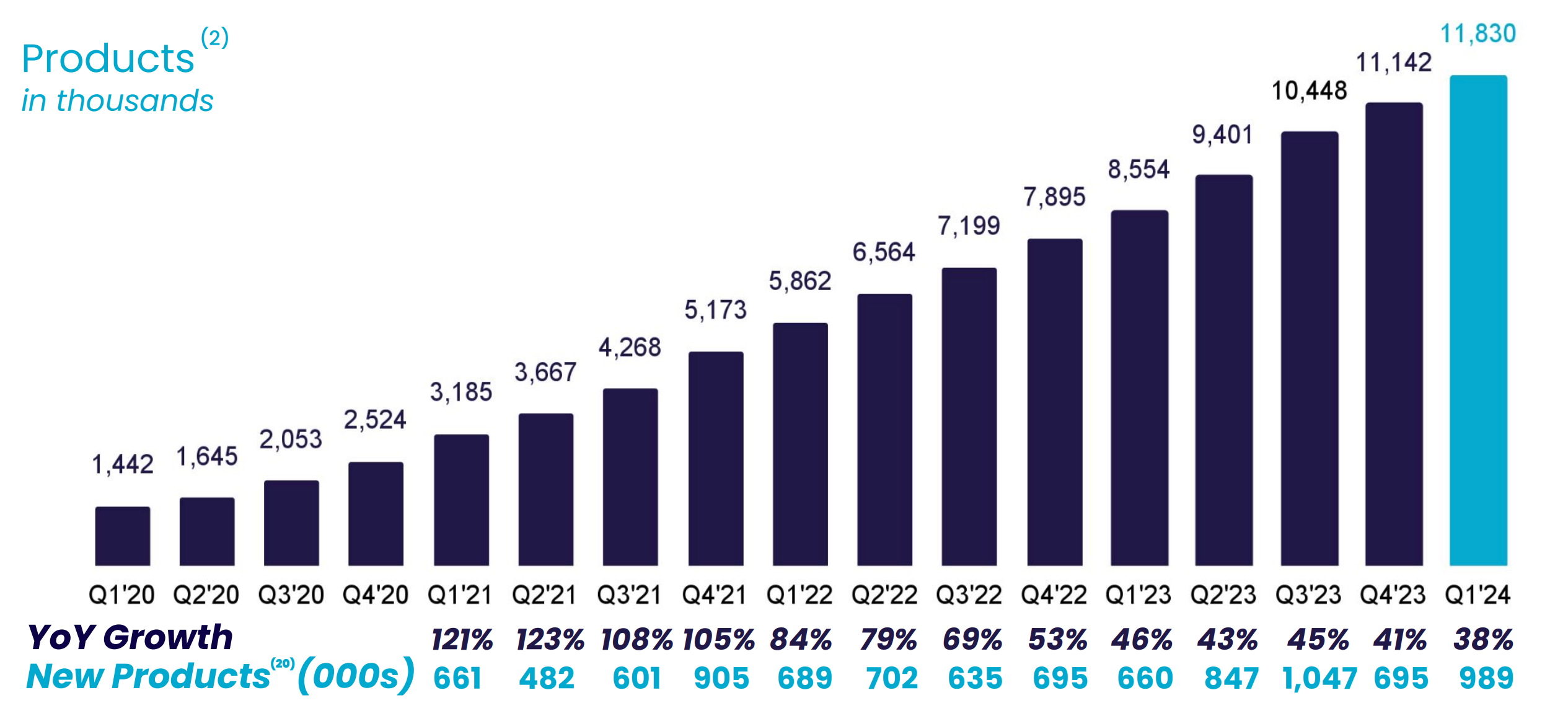

SoFi Total Products

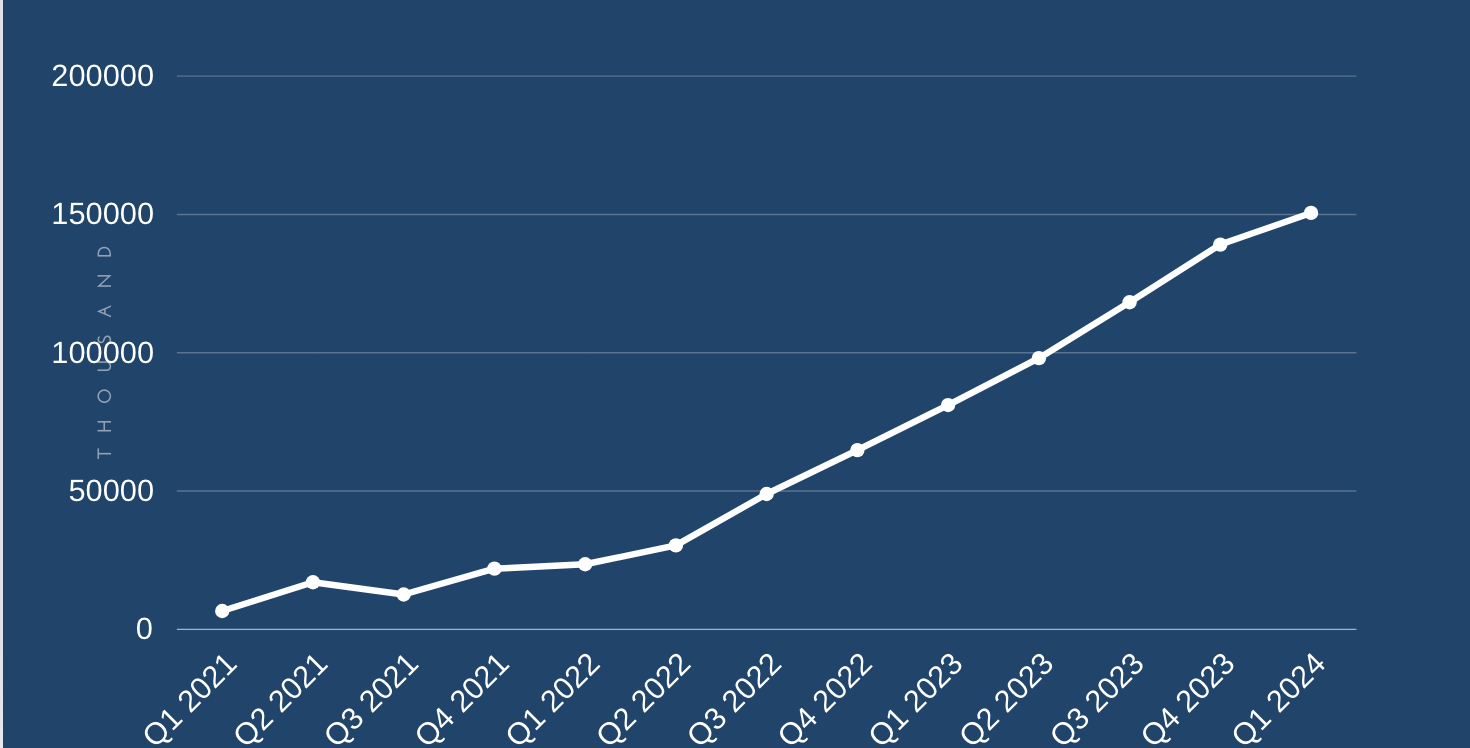

SoFi’s Total Products refers to the aggregate number of lending and financial services products that members have selected on the platform since inception through the reporting date, whether or not the members are still registered for such products. I personally find this bizarre and I do not know why they wouldn’t focus on total active products. A product that is no longer being used doesn’t generate revenue and therefore is a useless KPI. Given the obscurity of the metric and the required guess work, we will ignore it. Below you can see their product growth.

SoFi Lending - Business segment #1

To understand the business of banking, you need to understand the fundamentals of how loans work. A bank takes in customer deposits and then loans this money out. Between these two activities, you have what is called the net interest margin, or NIM for short. This is the the difference between interest income and interest expensive divided by the average earning assets. For example if a bank has an interest income of $5 million from its loans and investments, and it incurs an interest expense of $2 million on its deposits and borrowings. If the average earning assets for the period are $100 million, the NIM would be 5 million - 3 million / 100 million = 3%

The rate banks charge depends on the type and risk of the loan. Mortgages, for example, tend to have lower interest rates since they require a down payment and are also backed by the home itself, making them much less risky. A personal loan with no collateral, on the other hand, is much riskier and requires a higher interest rate to be worthwhile for the bank.

Another important metric in lending is the percentage of non-performing loans (NPL). These are loans the bank doesn't expect to be paid back and are written off as a loss, although they can sometimes be sold for pennies on the dollar to debt collection agencies. Banks need to balance NPLs with the net revenue generated from their lending segment in order to be profitable.

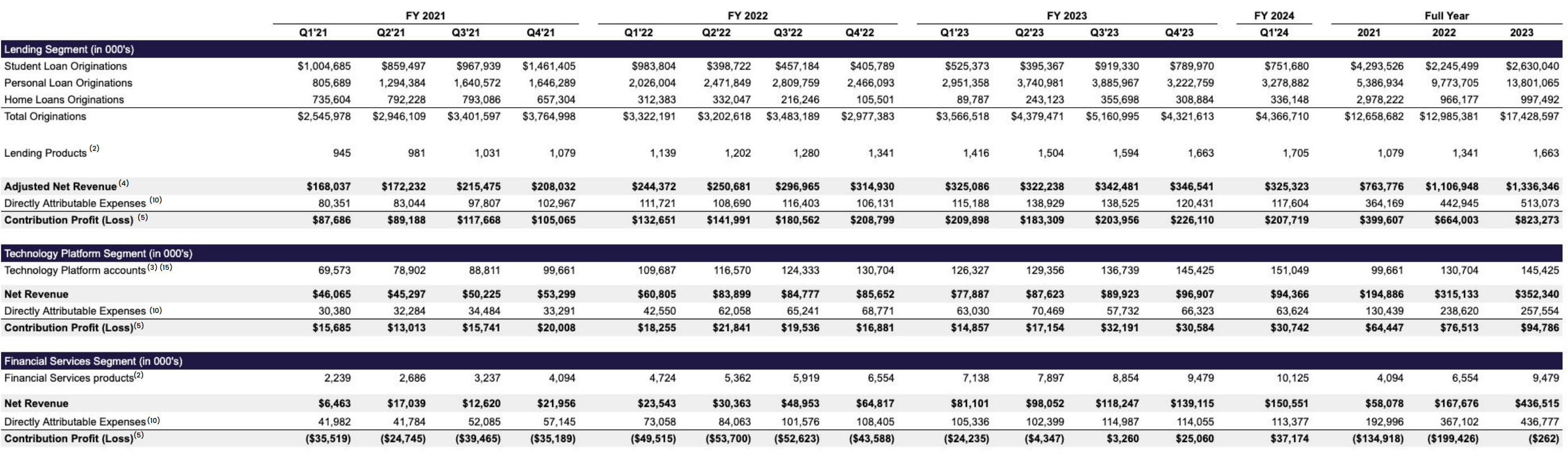

Right now, loans are where most of SoFi’s revenue is coming from. They offer the following loan types: personal loans, student loans, and mortgages, as well as refinancing services in all of these segments.

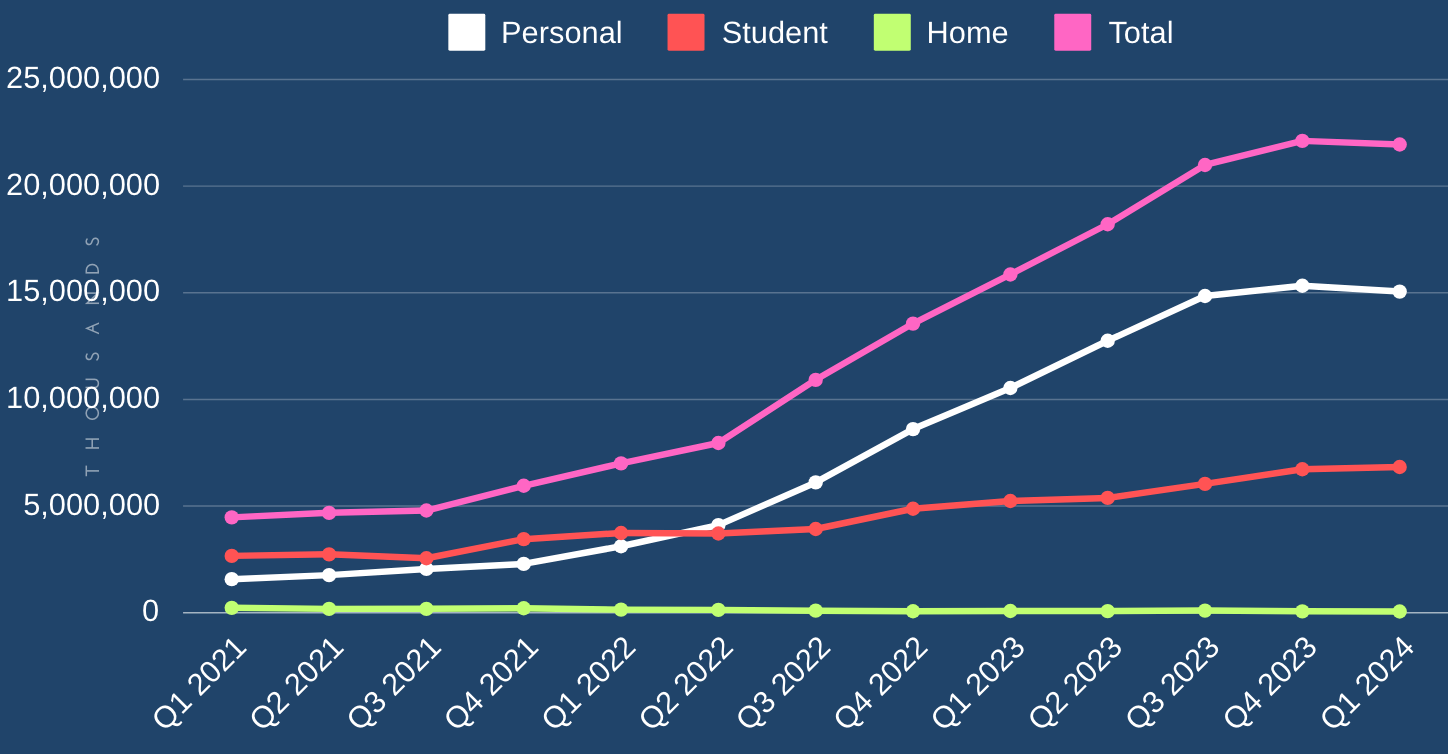

Loans Outstanding

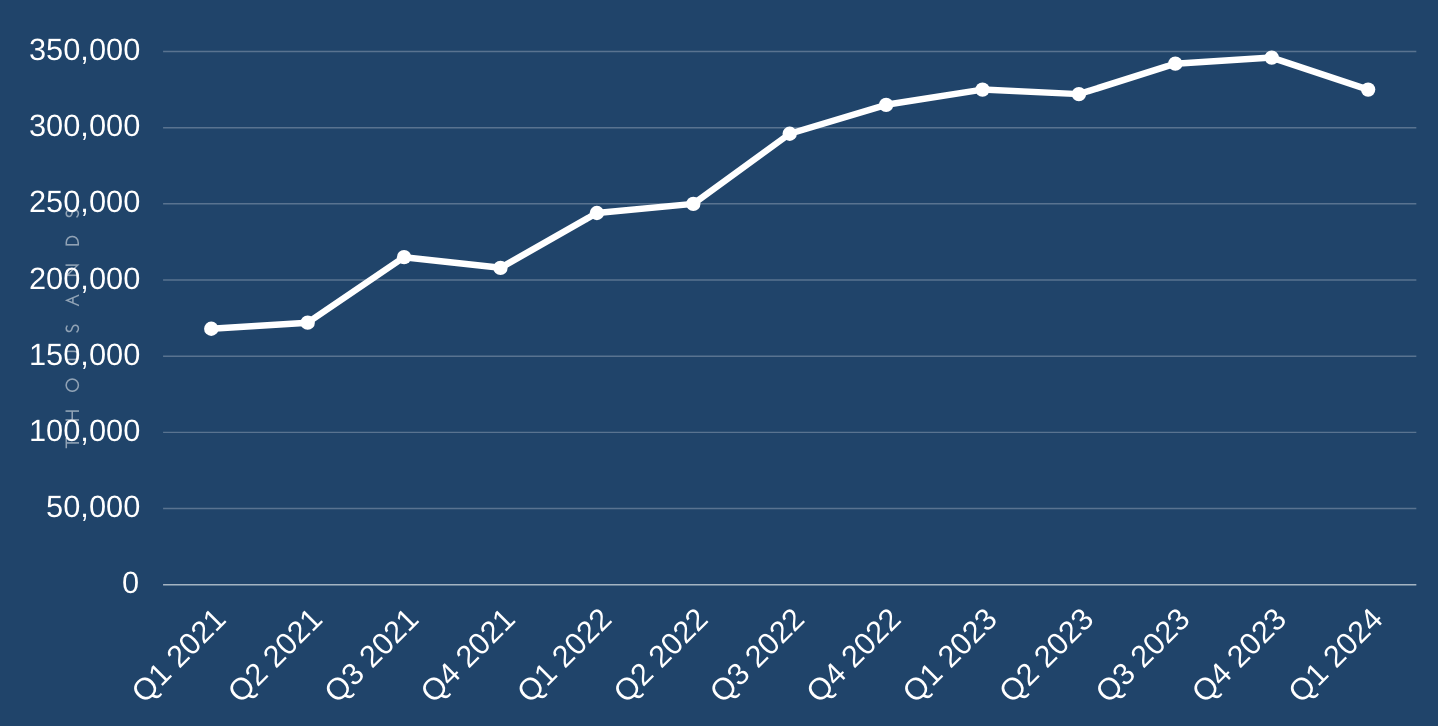

Adjusted Net Revenue

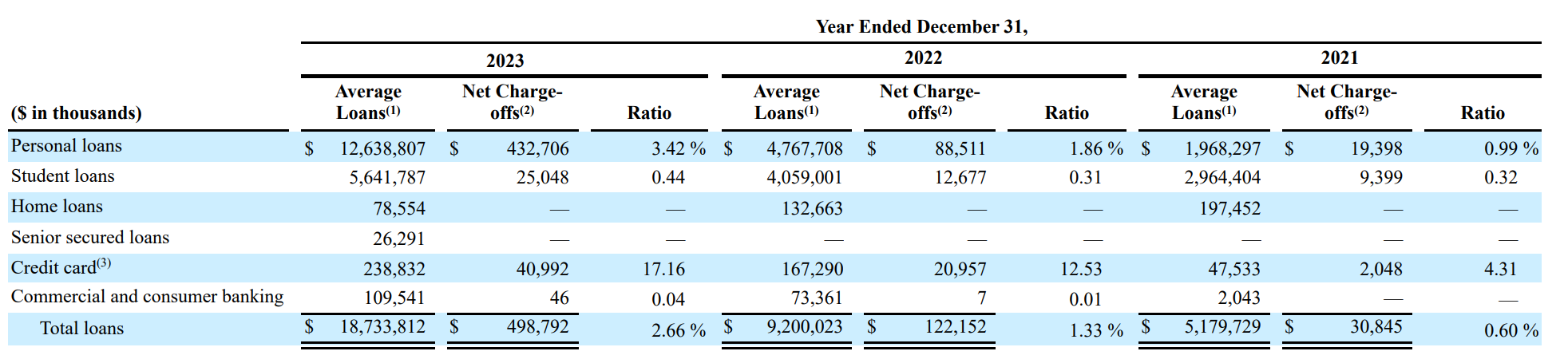

Loans make up about 50% of SoFi’s revenue right now, which is why many people refer to SoFi as a bank. A significant portion of this revenue is derived from personal loans. One advantage of personal loans is they typically have a better NIM due to the increased risk associated with them. Increased risk can yield increased profit to the bearer as long as the risk is calculated appropriately. To get a feel for the quality of these loans, we need to look at their net charge-offs.

2023 Net Charge offs

There are good and bad aspects of SoFi's net charge-offs. The good news is their current numbers are not that high, with 2.66% of total loans having a net charge-off. The bad news is that this number has been slowly increasing, which could mean that some of the older loans they issued were not of good quality. How concerning this is will depend on how 2024 goes. So far in Q1, they saw a minor reduction in net charge-offs to 2.65%. Ideally, this number remains stable because if it increases long-term, it suggests they might have a lot of bad debt. 2.65% is in line with their expectations so I don’t want to give the wrong impression here.

Overall, their loan book is solid, in my humble opinion, but I want to touch on a point that is true for all banks. It can be hard to determine the quality of a loan book during a bull market, as everyone is employed and can make their payments. In a downturn, people lose jobs and banks start seeing an uptick in delinquency. In 2008, many banks were carrying very bad loans and got absolutely hammered in the downturn. Because SoFi is a younger company, we don’t have a history of how their loans perform in a downturn. This isn’t to say their loan quality is bad, it’s just something to be wary of.

Finally, SoFi is slowing down their loan book growth this year due to macro concerns. While I don’t have any additional useful insights, it’s clear they have grown their loan book quite rapidly. It's better to take a long-term approach rather than focus on short-term profits.

SoFi Technology Platform - Business segment #2

The banking system is still largely built on legacy software written in COBOL and C. As a result, even massive banks still rely on this legacy software. Given the amount of regulation and compliance, the time and effort to migrate to newer technology are extensive, which is why many companies still use this legacy software today. This is where the SoFi technology platform comes in. The general idea is for SoFi to be the AWS of banking, providing banking as a service. It currently consists of two products: Galileo and Technysis. Galileo provides API-based solutions for card issuing, payment processing, account management, and fraud detection. Essentially, it allows companies (such as Robinhood) to quickly and easily issue their own credit cards. The business was acquired for $1.2B back in 2020. Technisys is a cloud-based banking platform that SoFi acquired for $1.1B in 2022. Anthony Noto (the ceo) essentially describes it as banking lego blocks that allow a customer to opt-in to pre-created banking solutions or build their own custom solutions.

Technology Platform Revenue

The most informative way to understand the effect of the platform’s revenue is to see its revenue overtime. It grew quite rapidly up until Q2 2022 and has leveled off a bit since. It’s also worth noting SoFi estimates that using their own platform for their banking services will have approximately $75 to $85 million in cumulative cost savings from 2023 to 2025 and approximately $60 to $70 million annually thereafter. Without hard numbers it’s hard to give anything concrete, but those savings will add up a lot over time. Currently the technology platform is about 18% of their revenue. It’s difficult to give a judgement on this investment because it’s still fairly new. It will be best to revisit this investment in 2030 ten years on. As it currently stands though, I would say it’s a net even with the revenue and savings they generate. If there is a critique it would be this segment distracts from there primary revenue drivers in the loan segment and financial services segment.

My only other note on the technology platform is that they are still sold as two separate services. AWS is one platform where each service plugs into another service. There shouldn’t be a Galileo and Technysis; there should only be a “SoFi Technology Platform.” These services should plug into each other, creating a much better experience from an engineering perspective. Ideally, as a bank, you have one website to manage your banking services and provision accounts for engineers. This is the most obvious value add to me in this segment. It would also make the cross sell of banking services much easier.

Financial Services Segment - Business segment #3

The SoFi Financial Services segment currently consists of the following products: checking and savings accounts, investing accounts, budgeting tools, and credit cards. Essentially, these are the products you offer to banking customers. Their revenue growth has been impressive, at 160% year-over-year from 2022 to 2023. At the end of 2023, they hit an inflection point where revenue exceeded costs for the financial services segment, turning this part of the business profitable. This is an ideal area to continue to grow because it directly relates to the loan part of the business. A long-term relationship with a customer provides insight into the quality of that customer, allowing SoFi to offer the best quality loans given the available risk profile. It also aligns with their mission statement of helping people achieve financial independence. It makes sense to have all your financial needs met through one portal as opposed to several separate financial institutions. That being said, this part of the business did see slower revenue growth between Q4 '23 and Q1 '24 at less than 10% quarter-over-quarter. SoFi has been intentionally tightening credit standards in 2024, and as a result, this is likely the source of their slowing revenue growth in this segment.

Financial Services Revenue

Financial services account for about 25% of SoFi's revenue currently and are their fastest-growing segment. I personally believe this is their best opportunity to diversify their revenue streams. Most impressive here is their deposit growth of $3B quarter-over-quarter to a total of $21.6B in total deposits in Q1 '24. This is good for SoFi because deposits are the cheapest form of money to lend on. As we saw above, most of their revenue comes from loans. So, what SoFi will probably do this year is build a solid deposit base, observe how their loans outstanding perform, and then, going into 2025, grow their loan portfolio consistently and responsibly. If SoFi does this well, for the first time in a long time, SoFi investors might finally see a strong return on their investment.

Another interesting point is the growth in SoFi Relay, which allows users to track and manage their financial accounts and investments in one place. This segment grew from 2.2M users to 3.6M users year-over-year. This product is very similar to Mint, if you have ever used Mint before. Mint has recently shut down, which I believe will drive a substantial user increase in Relay. The value add in Relay is not its ability to drive revenue growth but its ability to attract new users whom SoFi can cross-sell to through either bank accounts or credit cards. Relay also provides deep financial insight into each user, so it's possible SoFi can use that to get a better sense of the lending quality of each user as well. It will be interesting to see this segment develop over the year and to see how it contributes to the overall business.

As a whole, the financial services segment is at a turning point and I believe will continue to grow the fastest of SoFi's three segments in the next few years. Ideally, SoFi will drive both deposit and credit lending growth. If they do both successfully, it should drive very solid profits. If this business is struggling going into 2025, then I do think investors should be very concerned.

Segments Revenue Consolidated

SoFi’s Dilution

SoFi has diluted their shareholders quite a bit, and I want to touch on that here. First, we need to cover the fundamental issue with dilution. Anytime you purchase a stock, you are purchasing a percentage ownership of a business and, as a result, are entitled to both the existing equity in the company as well as future profits. If there are 10 shares outstanding and you own 1, then you effectively own 10% of the business. Now imagine if said company were to issue 90 new shares. You would go from owning 10% of the business to 1% of the business. In order for you to break even, you would need the price (and really the fundamentals of the business) to increase 10x just to break even. Anytime a company dilutes their shareholders, they can be hurting their owners.

SoFi went public with 794,692,813 shares outstanding and today are at 1,056,491,365 shares outstanding, representing a 32% increase. Now, dilution isn’t necessarily a bad thing if it drives appropriate returns to shareholders. However, in SoFi’s case, the stock has only gone down since the IPO. Their dilution has come through two key areas: acquisition and debt extinguishment. If you pay 1:1 for another company via your shares, in a sense, your increase in company value directly offsets dilution. So if you dilute by 10% but increase your company value by 10%, then you, as a shareholder, are not affected. It’s hard to judge the fair value of SoFi’s acquisitions, but if you feel they have gone up in value, then you are ahead; if you feel they’ve gone down, then you are behind.

The second aspect I want to touch on is their debt. Most of their debt is issued as convertible notes. Convertible notes essentially allow either SoFi or the investor to convert their outstanding debt into SoFi stock if they so choose at a set price. So even if the stock goes up 100-fold, you, as the investor, can convert at the set price. This can work in the company's favor if the set price is higher than the current price on the day of issuance. This is because the alternative to raising money would be to issue new shares and sell those directly on the market. So if you issue convertible debt at a higher price, you are essentially selling your shares for more. However, if the share price goes up a lot, you later on are taking a significant loss on those conversions since the set price for conversion would be lower.

SoFi extinguished a lot of debt last quarter by exercising their right to convert the debt to notes, which saved them a lot of interest but still diluted shareholders by over 10%. I would like to see SoFi extinguish their remaining debt and massively cut back on share dilution. As an investor, I avoid companies like SoFi because of how much share dilution hurts the investor. If you want to know why the company is trading sideways, reread this paragraph. Their gains are constantly offset by their dilution.

Conclusion

SoFi is a legitimate business that is finally turning the corner on profitability. They are estimating to achieve about $100 million in net income this year. Most banks are typically valued based on price to book (P/B), and SoFi is currently at a P/B of 1.2 when considering intangible assets and 1.8 when considering only tangible assets. Therefore, I believe their true P/B is probably around 1.5. Given their risk, this is a bit high, but their growth potential factors in here. The best way SoFi can reliably deliver returns to their investors is to continue growing their tangible book value. SoFi is estimating $800 million to $1 billion in book value growth for the calendar year of 2024, which is about a 15%+ increase from the year prior. It’s also worth noting that SoFi is intentionally slowing loan growth this year due to rate uncertainty. It will be interesting to see how they choose to scale their book value in 2025, which could be a big year for them to finally have the stock start consistently trending upward.

For me personally, I still won’t be investing in SoFi for a few simple reasons:

While their stock dilution has probably been necessary to some extent, I am worried this trend will continue. I want to see them get their dilution under control and, ideally, start reducing shares via buybacks.

They are hitting profitability, but they still need to ramp up revenue considerably. Ideally, they should keep expenses relatively flat while growing revenue that falls to the bottom line. I want to see how they manage this over the following year.

Finally, I simply think the company is probably priced around where it should be, and as a result, I don’t feel I would have a great margin for error here. If SoFi continues to go sideways while their fundamentals improve, I would then start becoming interested in investing.

I understand the interest in this company and why so many people are bullish on SoFi. I’ll keep an eye on them and will do an article 1 year from now to see how things have progressed. I have changed my mind on SoFi and I do think despite the SPAC they are legit and will do well long term. As always, only time will tell.

Sources

https://d18rn0p25nwr6d.cloudfront.net/CIK-0001818874/a31f2915-31bf-45ae-99cf-18f3c0138869.pdf

https://s27.q4cdn.com/749715820/files/doc_financials/2024/q1/Q1-24-Investor-Presentation.pdf

https://www.sofi.com/press/sofi-to-acquire-technisys

https://s27.q4cdn.com/749715820/files/doc_financials/2024/q1/c8157c1f-0d4f-406f-b32b-575af8ef7f3f.pdf

interesting read Alexander, really interesting that you changed your POV and you dare to write it! I started to invest on the company 3 month ago via leaps jan 2026. small position but i am increasing it last weeks.