The Bancorp, Inc

Disclaimers

This is not financial advice, I encourage you to do your own research

I am long on TBBK at a cost basis of $33.22 with 100 shares (probably will add more)

The Bancorp, Inc Numbers

Price $34.13

Market Cap $1.70B

P/E 9.29, P/B 2.0

5 Year CAGR 30%

I recently came across a website that tracks insider buys, you can find the website here. A lot of the companies I came across were obviously beaten up a bit and potentially had value, but were pretty average companies otherwise. It was clear to me that some would make some solid cigar butt plays but I also felt that there was a clear and obvious downside to many of these companies. Then I came across a bank I never heard of called The Bancorp (TBBK) with a wall of insider buying (6 Unique individuals, $3.9m for the year)

Image from StockUnlock

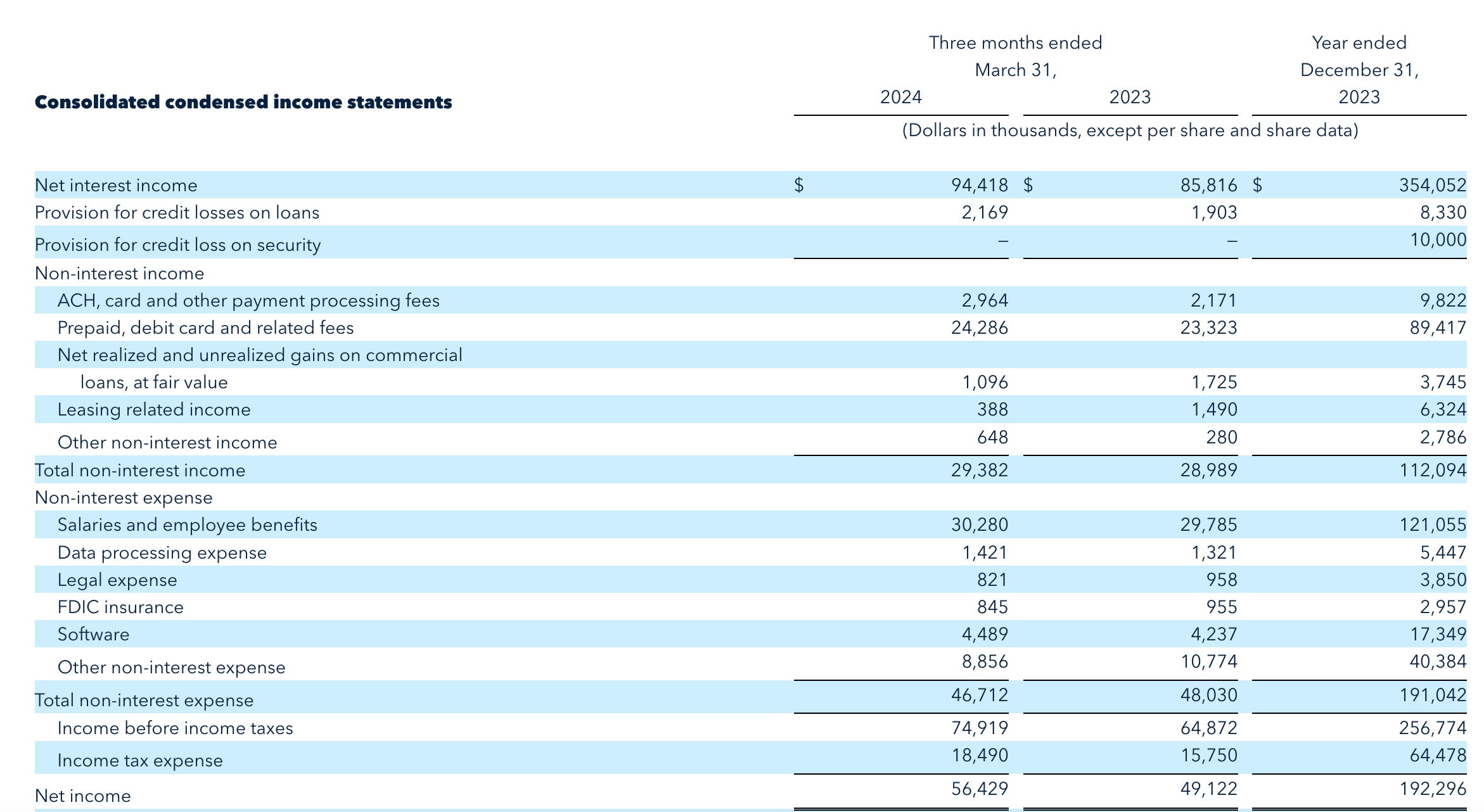

To be clear there’s actually a lot of publicly traded banks with insider buying, so I would never take this as a hard signal but rather a hint that something interesting might be going on here. What I found is extremely simple but powerful: TBBK is just a very well run bank with very strong numbers across the board. The easiest way to understand this is from their recent earnings presentation here. The below slide is the best summary of their earnings so I will break it down line by line here.

Figure 1 - The Basic Numbers

Return on Equity (ROE) - Return on Equity is calculated by taking Net Income / Shareholder equity. The real purpose of this metric is to demonstrate how good management is at compounding shareholder equity. If management drives revenue growth but their ROE is 3% then they might as well redistribute those funds to shareholders who can earn better returns buying bonds. Essentially it would mean for every $100 of equity they are only earning $3 if ROE is 3%. As we can see management over the last 3 years has been driving 18%+ ROE and was able to hit 28% in Q1 2024. Essentially for every $100 of equity, they are returning $28 annually. These are very strong numbers and it indicates management is great at compounding value for their shareholders

Return on Assets (ROA) - This is a commonly used metric in the banking world to show how good a bank is at utilizing their assets, most banks average between 1%-2%. We can see that TBBK hit 3%, which is well above the Q1 2024 banking average of 1%.

Earnings per share (EPS) - This is a very simple metric, it’s just net income divided by shares outstanding. It represents the earnings you are entitled to for each share you own. TBBK has been comfortably growing EPS at well above 20%+ YoY since 2019. They are targeting $4.25 this year without accounting for share buybacks. Given they hit $1.06 ($1.06 * 4 = $4.24) this quarter this seems very achievable by simply maintaining their current business. $4.25 is a 21.7% increase YoY.

Bancorp Bank, N.A. Leverage Ratio - This is just a measure of a bank's capitalization relative to their assets. It helps determine a bank's ability to absorb losses on non performing loans. The well capitalized minimum is 5%, so TBBK are over double the legal requirement. In a downturn they should be well positioned to absorb losses should they occur. This does give us valuable insight into their responsible loan allocations. The image below does a good job of showing their capitalization strength relative to legal requirements.

Figure 2 - Capitalization Ratios

Total Assets - We can see this number has been flat in figure 1. This is likely because 2022 to 2023 there has been a lot of uncertainty and increasing interest rates. They’ve also been using their capital to do buybacks. If they are spending capital then they can’t do more loans without reducing their leverage ratio. So in general it makes sense to keep this flat if returns are being driven via reduced costs and increased EPS.

Efficiency Ratio - The efficiency ratio is calculated using total non interest expense divided by a bank's total revenue. It represents how efficient they are in terms of earning revenue. Essentially for every $1 of revenue they spend $0.38 earning that revenue. What’s notable here is that number has decreased quite a bit since 2021 and this is what is driving their earnings growth. Most banks are between 50% - 60% for their efficiency ratio. 38% is extremely good and well below the industry average. This means most revenue increases are dropping straight to the bottom line as income. TBBK has achieved this by leveraging technology as they scale. Essentially it helps keep their costs down while servicing more customers.

Share Buybacks

TBBK had 58.8M shares at year end of 2021 and have reduced this share count to 51.76m shares outstanding at end of Q1 2024 through aggressive buybacks. At the Q4 2023 earnings call they said this year they plant to do 50-100m of buybacks per quarter. They retired 1,262,212 at a cost basis of $39.61 in Q1 of 2024 and they plan to do $100m of buybacks this quarter Q2 2024. If the share price stays constant than they can retire 3m shares this quarter or nearly 5.6% of shares outstanding. If they maintain this rate of repurchase we could see a total reduction of over 10m shares this year or 18% of shares outstanding. Management mentioned on the Q1 2024 earnings call that they felt the shares were underpriced and are committed to doing aggressive buybacks at the current price. This leads to the following math

Management forecasts $4.25 EPS this year was not inclusive of share buybacks. They did $56.4m in income in Q1 2024, so the yearly income calculated below seems very realistic. They reaffirmed this target at end of Q1 2024

Management has spent 50m in Q1 on buybacks and provisioned another 100m for Q2. At current prices that will be 3m shares for the quarter. The price also has never gone above $50 a share. So we can assume they will average 1m+ a quarter pretty easily this year unless the price jumps

They started the year with 54,204,930 shares outstanding

54,204,930 shares outstanding * 4.25 EPS = $230,370,952 income for the year

They are at 53.3M shares at the end of Q1 from buybacks. To make the math easy, we will assume they average 1.1M a quarter and hit 50m shares by the end of this year. This is conservative at their current share price and they will likely have less shares than 50m.

$230,370,952 / 50m shares outstanding = $4.60 EPS

This a 31% increase YoY for their EPS from $3.49 the year prior. If they don’t manage any buybacks but deliver on $230m of income then they will realize about 21% YoY. So I think with the buybacks it’s quite likely that even if they miss the income target they hit 20% YoY on EPS again. The longer the price stays at roughly $33 the better as they can reduce their shares outstanding massively with aggressive buybacks driving EPS. At the extreme end they could achieve $5 EPS if the share price remains constant through the end of year.

Figure 3 - Revenue Breakdown

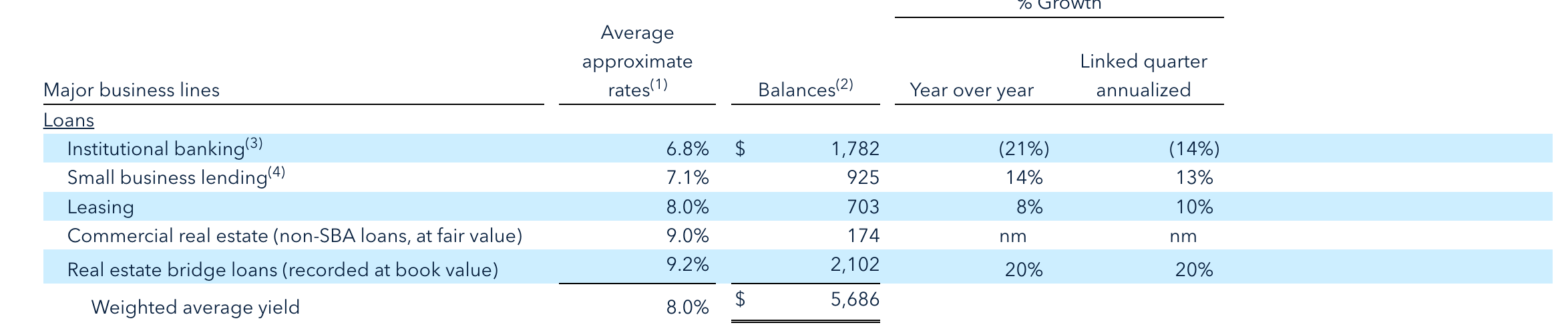

Figure 4 - Balance Breakdowns and Average Rates

The majority of the bank's income is from their Net Interest Income. As I said, TBBK is really just a bank. I don’t plan on covering the various loan types and will refer you to their recent 10Q to learn more. I do however think it’s worth looking back at their historical performance in terms of NPL.

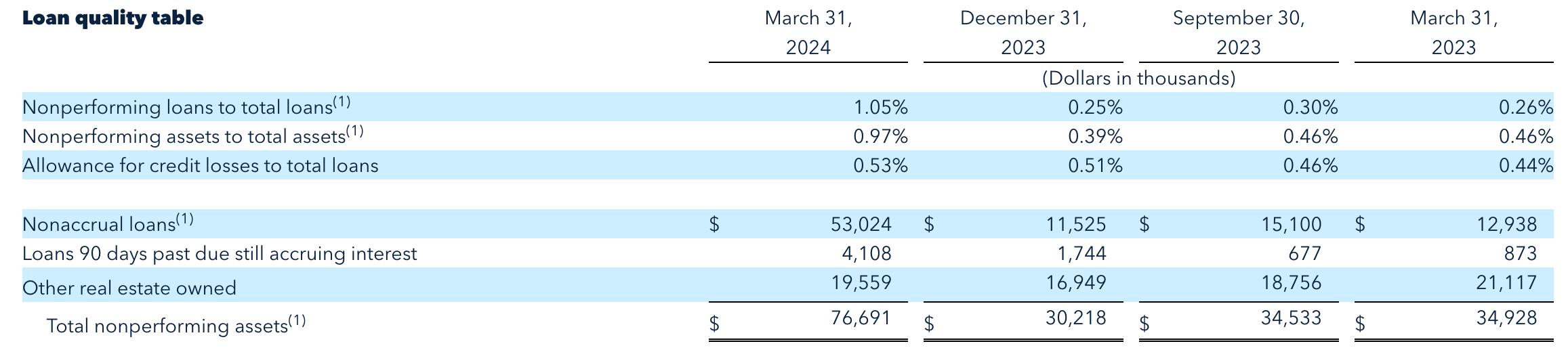

Figure 5 - Last year Non Performing Loans

A net charge off is essentially how much money banks have lost on loans each year. Of all their numbers, this is one of the most important areas to touch on. As you can see in figure 5 there has been a major uptick in the last quarter of their non performing loans. They mentioned there was an initial wave of bridge loans needing adjustment which has stabilized as of now. Currently all loans are at an 80% Loan-to-value (LTV) which gives them a solid buffer if they were to repossess more of these properties.

They had one major apartment that became NPL and is the major contributor to the above numbers and which TBBK explained as follows

In the first quarter of 2024, a $39.4 million apartment building rehabilitation bridge loan was transferred to nonaccrual status. On April 2, 2024 the same loan was transferred from nonaccrual status to other real estate owned (OREO). We intend to complete the improvements, which have already begun, on the underlying apartment building. During the time that improvements are being completed, the Company intends to have a property manager lease improved units as they become available, prior to the sale of the property. The $39.4 million loan balance compares to a September 2023 third party “as is” appraisal of $47.8 million, or an 82% “as is” LTV, with additional potential collateral value as construction progresses, and units are re-leased at stabilized rental rates.

Essentially they believe they can sell the property for $47.8 million today. On the Q1 2024 earnings call they mentioned they are exploring potential offers but in the meantime plan to finish the repositioning of the property themselves. They currently aren’t looking to capitalize on this project and will sell it if a break even opportunity comes up. They currently estimate several quarters to finish this project.

Is this a concern?

Damian Kozlowski the CEO said the primary cause of this non performing loan was the combination of both high interest rates and inflation brought on by covid coming from loans given out in the 2021 time period. Paul Frenkiel (Chief Financial Office) said that a 3rd party appraisal put all loans at 79% LTV as-is. This means with no further repairs the loans are 80% of the properties currently valued. So if they should not perform, they can sell the properties to other buyers looking to finish the renovations. This is definitely something to keep an eye on over the following year. In general TBBK has done well historically in this area and given both their capitalization rates as well as LTV they are in a solid spot to avoid any potential losses. I do think if this was becoming a major concern going into Q2 we would not have seen that wall of insider buying

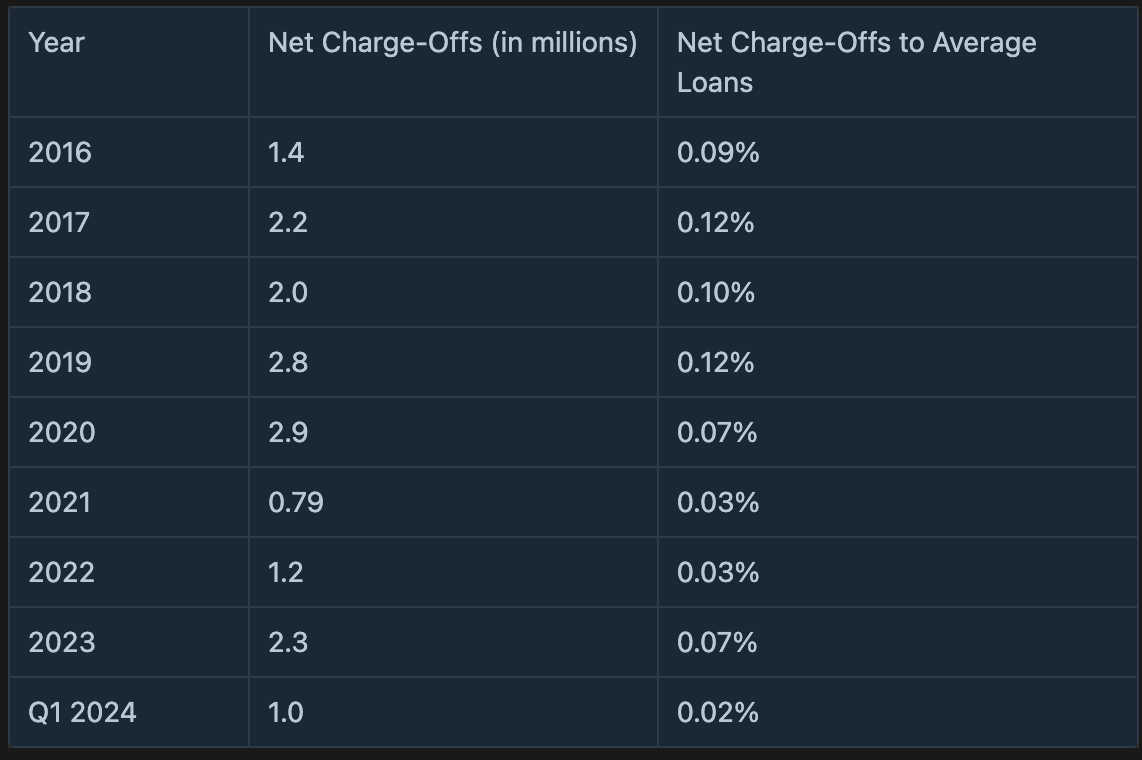

Figure 6 - Yearly Net Charge Offs

Historically they have done very well in terms of net charge-offs, often average below 0.1%. If they had higher historical averages or there was a large number of properties becoming NPL I would be more concerned. I believe TBBK has done a good job of managing this historical risk and are in a good place going forward.

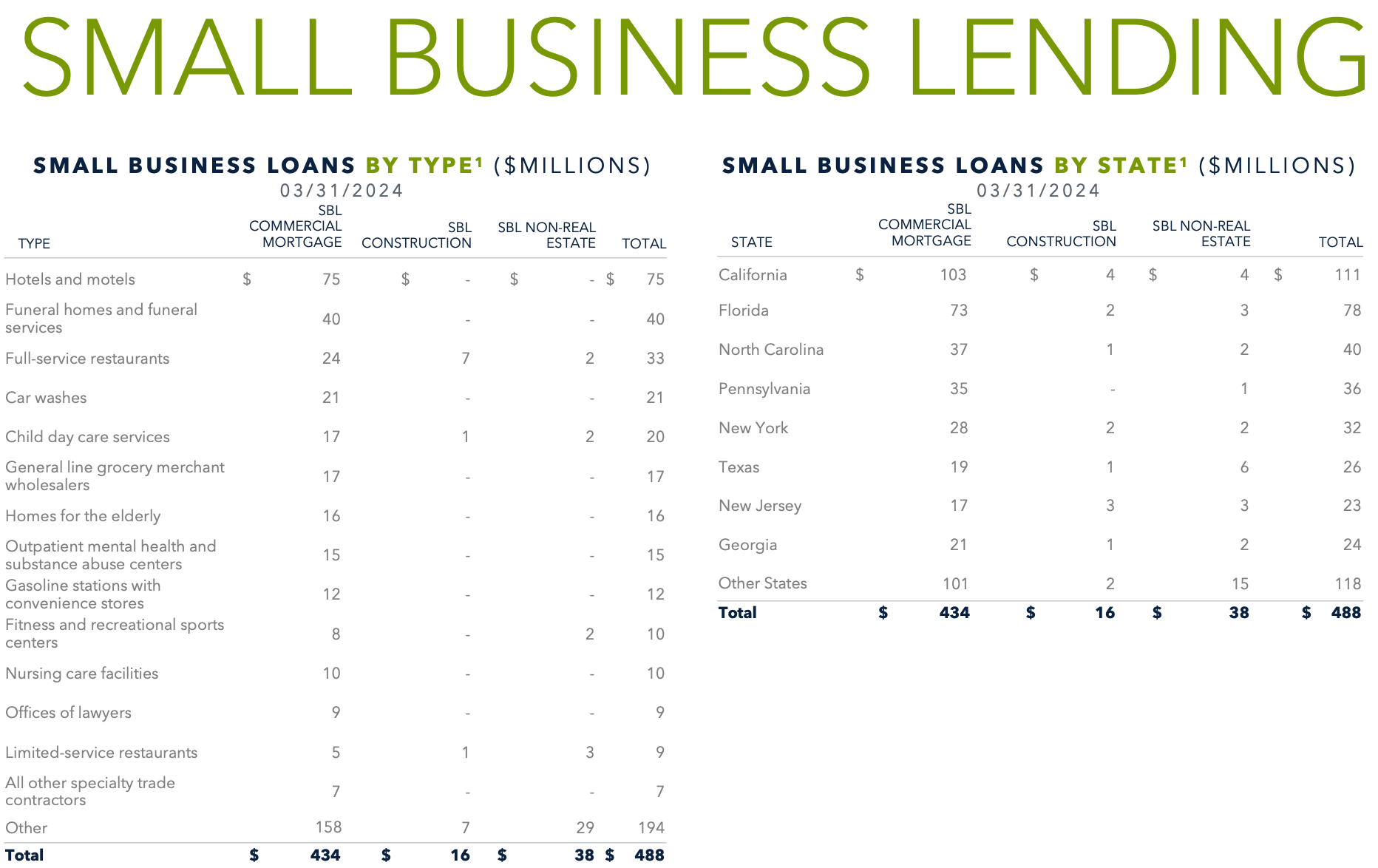

Figure 7 - Small Business Lending Portfolio Makeup

Figure 8 - Commercial Fleet Leasing Portfolio Makeup

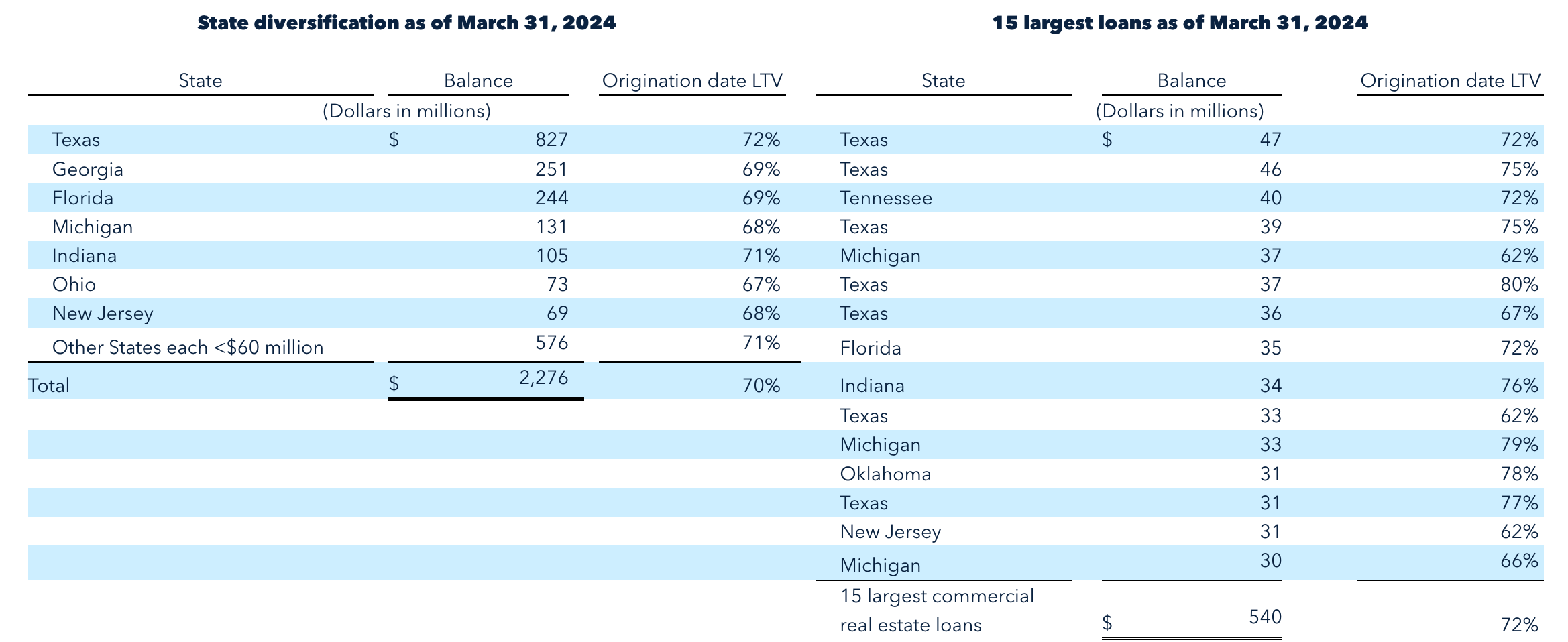

Figure 9 - Real Estate Bridge Loan Portfolio Makeup

The last thing I want to touch on is in regards to their loan diversity. While TBBK is a regional bank they are currently lending nationally and across numerous different markets. This is important for risk diversification as a downturn in a regional market can hurt a bank significantly. They intentionally try to be smart about their loan business in terms of diversification as well as lending to folks with a strong financial profile. I also want to note their LTV (see figure 9) on many of these properties are 80% and below giving them solid breathing room in case any of these property loans go into foreclosure. For a full overview of their loan types and locations, I recommend taking a look at their Q1 2024 press release.

TBBK NIM

TBBK NIM is currently around 5% up from roughly 3% just a couple of years ago. This increase has been driven by a couple of things. First the overall interest rates have increased more than the rate of their cost of funds. Their cost of funds went from roughly 2% to roughly 2.5% while yield on their assets has gone from 3.6% to about 7.5%. They also increased their loan book quite significantly in areas that have higher yields which drove up their average yield. They are currently building a fixed rate loan portfolio at roughly 5% since they believe we will start to see rate cuts by early next year. If rate cuts occur it would actually increase their NIM since most of their loans are at higher rates. I think in general while we could see a minor reduction in NIM long term the 3% was largely driven by record level fed interest rates of the early 2020s time period and we should see more mid 4s to low 5s going forward in terms of fed interest rate. This is something to keep an eye on long term. A decrease in NIM would affect their profitability and as a result their EPS.

Partnership with Block and fintech segment

They make non-interest income by issuing prepaid cards and debit cards for large businesses. Of the 466m in revenue for Calendar year 2023, 112m of it was through their prepaid debit card solution. They partner with big companies that want to issue these cards for employees who need access to capital for employee transactions. Their business has grown steadily and saw a 10% YoY increase YoY in Q1 2024 quarter. This additional revenue stream is good for diversification of income and helps make the business less prone to the ebbs and flows of the interest rate economy. In Q1 they also announced a new partnership with block which is as follows:

We are pleased to announce Block, Inc. (“Block”) as a new partner to our tech solutions ecosystem. The addition of this new relationship as well as the continued organic growth of the current portfolio should result in meaningful increases to the ACH, card and other processing fees line item.

They didn't give too much guidance on exact numbers other than this will start impacting revenue next quarter and will ramp up over the next few quarters. They plan to add 3-4 big partners a year. The real value add here is diversification of income outside of just lending. This is definitely an area to keep an eye on and see how the business progresses over the couple of years.

Conclusion

TBBK 2030 plan

Revenue: 1B

ROE: 40%

ROA: 4%

Capital ratio > 10%

Outside of the obvious returns for the next year, this is their plan for 2030. I think at their current growth rates these numbers are fairly achievable. I believe the current stock price should be between $40-$45 given their share buybacks and EPS increase. If they achieve their 2030 goals we would then expect to see a doubling of the current price to $80-$90. At current price today of $33 this would yield roughly a 20% annual compounded growth rate. It’s worth noting this is just a projection which means it’s possible they do not reach these goals. I believe given their current price, TBBK is a fairly straight forward value play. As always, only time will tell.

Source

https://investors.thebancorp.com/overview/default.aspx